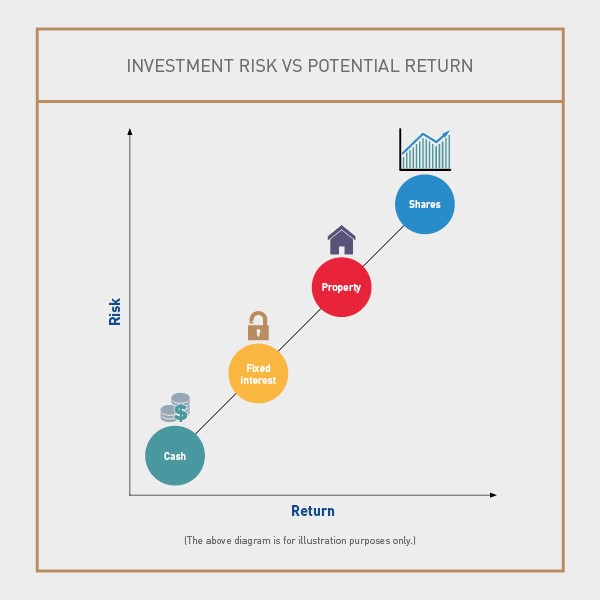

For investors, understanding the relationship between risk and return is critical: The higher the relative risk of an investment, the larger the possible return. With some asset classes the risk is small (cash, for example), while other asset classes (such as equities) involve a higher level of risk. However, even with traditionally safer investments, risk is never completely absent and returns are never guaranteed completely.

Even within asset classes, the level of risk (and potential return) may differ. Take equities, for example. Investing in a large blue-chip utility company will present divergent levels of risk and potential return when compared with a mining exploration company that drills for gold in central Africa. In the former, earnings and growth are somewhat predictable, which would typically mean a relatively lower level of risk, but the potential return is likely to be lower. With the mining exploration company, the level of risk is probably elevated (the company may not be producing earnings, for example), but your possible reward is in all probability higher.

“Understanding the difference between volatility and risk is also important,” says Warren Ingram, executive director at Galileo Capital. “If an investment is volatile, it’s not necessarily risky. Keeping your money in cash is highly risky as you are not going to beat inflation.”

“If you want your capital to beat inflation, you are going to have to embrace an investment that’s volatile. This gives you the best chance of beating inflation as long as you are patient.”

There are three main factors to consider when determining your risk preference and creating (or fine-tuning) an investment strategy: diversification, personality type and time horizon.

Don’t put all your eggs in one basket

The primary strategy to manage risk is diversification. This is not a guarantee against losses, but should provide the best possible returns over the long term, at the lowest amount of risk. Your portfolio should be spread among different asset classes, such as cash, bonds, property and shares (equities).

Options like balanced unit trusts offer this diversification in a single investment because the fund managers effectively make these allocations for you. However, you should also be diversified within the equity universe. It is no use sticking to only one type of company (blue-chip utilities, for example) or one sector or industry.

“Beyond diversification, across and within asset classes, one needs to be diversified over time as well,” says Ingram. “If you’re investing in lump sums, you should consider spreading that investment over months. This means your cost of entry will be averaged over time.”

Understanding your appetite for risk

Diversification is only one tool to manage your risk. The other two factors to consider are related to you.

The article Understanding your financial personality can pay dividends showed how knowing your personality type can make you a better investor. Simply put, if you are more cautious, you would need to actively take more risks. As Peter Dempsey, deputy CEO of the Association for Savings and Investment South Africa, pointed out in the article Financial advice critical in volatile times, loss aversion (falling prey to inaction or taking only timid action) can reduce the value of your investment portfolio. The opposite is also true; if you are fond of taking risks, you should deliberately be more conservative in your investment decisions.

Knowing your investment personality is also useful in understanding how you will react to certain situations. A risk-averse investor might have been tempted to cash out of equities towards the bottom of the market following the crash in 2008. This would have been a negative decision for future returns.

“I would argue the biggest stumbling block to investment success over time is that most people are extremely optimistic before they start,” says Ingram. “When markets drop, that’s the first time they understand their tolerance of risk. At that point they’re faced with the choice of either staying in or cashing out. Most choose the latter, which results in a permanent loss of capital.”

What is your time horizon?

Time horizon is the third element when establishing your risk appetite. Central to this is your age. The younger you are, the more risks you are able to take. And as you approach retirement, your risk tolerance necessarily reduces.

This is not an arbitrary correlation. The amount of money you can afford to lose in a temporary blip like a stock market correction is related to two things: your age and your net worth. You only need to look back at the 2008 global financial crisis to understand just how suddenly markets can move.

At age 40, you can recover from a 25% drop in the value of your equity portfolio, as you still have at least two decades of working and saving left. The picture is very different at age 60. One rough rule of thumb is to subtract your age from 100 and ensure that this percentage of your portfolio is invested in shares. So, if you’re 30, you’d be looking for at least 70% equity exposure (some advisers argue that you should subtract your age from 120). This is a guide that provides a useful, practical way of figuring out how your risk tolerance should change over time.

But age should not be looked at in isolation. Your net worth also needs to be considered. A R100 000 equity portfolio is worth more to someone with a net worth of R1 million than it is to someone with a net worth of R10 million. For the former, it’s 10% of their net assets, while for the latter it’s only 1%.

Your time horizon is not necessarily always related to retirement. You could be saving for your children’s education. With a time horizon of anywhere between 10 and 20 years, you should be far more comfortable with taking risks than when saving for a deposit on a property that you’d like to buy within one year.

In a paper for the CFA Institute, the organisation’s director of investor education, Robert Stammers, argues that one of the most common mistakes made by investors is “taking too much, too little, or the wrong risk”.

Understanding how much risk you are comfortable with and how much you are actually taking is crucial. The simplest way to manage this over time is to perform a regular check-up of your portfolio – possibly with the help of a financial adviser. Achieving a suitable balance between risk and return will ensure that you have the best chance of achieving your financial goals.