A rapidly changing world is creating new risks to retirement planning

Retirement planning has always faced uncertainty. Whatever your plan is, it can be affected by unpredictable factors, like your investment returns, inflation and longevity. "In addition," says Discovery Invest's Head of R&D, Craig Sher, "we are now vulnerable to new risks that affect our retirement journeys."

The chances of outliving your retirement savings are rising

In 1900, people lived for about 31 years. By 2016, that figure rose to 72 years. The United Nations predicts that global life expectancy will reach 77 in the next 25 years, and may reach 83 years within the next 50 years. That means we should expect to live about 5 to 10 years longer than our parents did.

But the average is not what kills a retirement plan - it's the extremes. Of today's South African workforce, around 800 000 are expected to live beyond age 100. Beyond these predictions, advances in medicine and technology will keep improving the length of the average life.

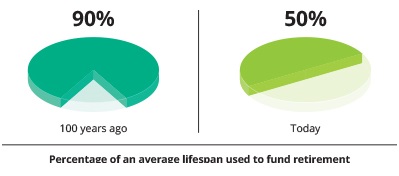

Sher highlights the fact that the portion of our lives in which we work and fund our retirement isn't increasing along with longevity.

With this trend on the rise, all bets for a regular retirement plan are off. The obvious solution is to work longer. "Deferring retirement for a year can take you one year into retirement without drawing an income, plus one and a half years' extra income from investment growth with a shorter post-retirement term - which means you could live for an extra two and a half years without your savings running out," explains Sher. "But a second risk brings significant extra uncertainty to the hopes of working for longer."

Unhealthy people experience the worst of both worlds

As medicine and access to medical care improves, people are able to live far longer in a poor state of health than in years gone by. 'Healthy Life Expectancy' is a measure of the number of years lived in a 'healthy' state, and is calculated by combining traditional mortality data with information on ill health and disability.

Studies show that Healthy Life Expectancy is increasing at a far slower rate than the traditional measure of life expectancy. According to Sher, this is doubly problematic for the unhealthy because:

- You still need to be able to provide an income for roughly as many years as the healthy.

- Your living costs will be higher due to higher healthcare costs. Before retirement, this makes it harder to save. After retirement, this increasingly eats into your income because healthcare inflation is higher than average price inflation. Sher explains, "For an average 25-year-old, the portion of their income being spent on health-related expenses increases nearly fourfold by age 65. Then to fund a mid-range health plan for 20 years in retirement, they'll need just over R3 million. But these costs depend to a large degree on their health. In Discovery's insured population, hospital costs for engaged Vitality members are up to 40% less than non-engaged members.

Offer

Discovery products recommended for you

You can get maximum boosts on your recurring contributions.

Get up to 50% extra retirement income for healthy living. For life.

This article is meant only as information and should not be taken as financial advice. For tailored financial advice, please contact your financial adviser. Discovery Life Investment Services Pty (Ltd): Registration number 2007/005969/07, branded as Discovery Invest, is an authorised financial services provider. Product rules, Ts and Cs apply.