Calculating your net worth is important because it helps you understand your financial health at a point in time, by providing an accurate indication of whether you have more (or less) assets than debt. This can help indicate how close you are to achieving a debt-free retirement – one of the key goals of retirement planning - and whether you are on target to building up enough assets to provide a suitable retirement income.

Focusing only on your assets ‒ or only on your debt – provides only one half of the picture. Instead, the difference between your assets and your debt gives a clearer indication of where you stand. As Discovery financial adviser, Louw Venter, explains, retirement planning aims to get an investor to retirement without debt – and knowing your net worth can help show how close you are to this goal.

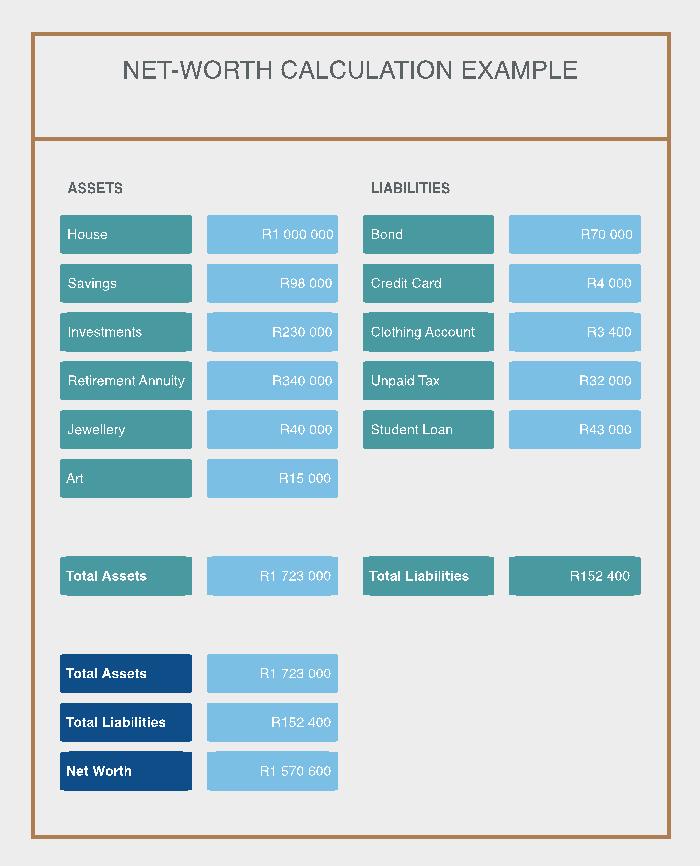

Calculating your net worth

Calculating your net worth is relatively simple: List the value of all of the assets you own, including your house, investments, savings, retirement funds and other assets. (The jury is out on whether cars are included given that it’s a depreciating asset. Some financial advisers do, others don’t.) From this total of assets, subtract all of your liabilities. For the average person, this would include a home loan and other debt such as credit cards and personal loans.

A useful signpost

“The net worth calculation is important in the context of retirement planning,” says Warren Ingram, the executive director of Galileo Capital. “Ultimately you want to get to a point where you have sufficient assets to fund your monthly expenses once you’re retired.”

Remember the 4% rule? William Bergen’s famous calculation can be used to indicate the amount you need to accumulate to provide a suitable income for at least 30 years. Calculating your net worth can show you how far or close you are to this goal.

Take 50-year-old Joe as an example. He has calculated that he needs R16.2 – million saved at retirement to give him an annual income of R648 000. If Joe works out his net worth on a regular basis, he can tell how close or far away he is to that R16.2-million goal, and whether his net worth is increasing over time in order to achieve that goal.

The value of tracking net worth

Ingram adds that net worth in isolation is not as important as measuring it regularly and keeping track of its movement from one year to the next.

“If your net worth is increasing, which it should be, your position is improving from a financial and retirement -planning point of view.”

As Venter points out, a successful retirement strategy requires that your income leads to a debt-free, income-generating asset base, and monitoring your net worth over time can indicate whether your assets are growing and your liabilities are reducing.

If your net worth flatlines or reduces from one year to the next, you need to understand why, says Ingram. “Is the stock market down? That is no reason to panic.” If your debt has increased, you want to look at it more closely. Typically, flatlining (or worse, declining) will mean you simply aren’t accumulating enough assets. For most people that means not saving or investing enough.

“The classic mistake is to focus on the asset side of the equation, and people rush to try rather invest more,” says Ingram. “But debt compounds against you. Looking to beat prime (at 10.25%) is a tough ask.”

For more information on investing for retirement, speak to your financial adviser.

This article is part of an investment series by Discovery Invest.

Discovery Invest is an authorised financial services provider. Registration number 2007/005969/07. For more information on Discovery Invest, contact your financial adviser.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell investment funds.